If you’ve ever sat and asked yourself, “can you get a mortgage with an IVA?”, you’re not alone. Many people assume that an individual voluntary arrangement (IVA) automatically rules out homeownership, but that isn’t the full story. In 2025, it’s still very possible to get a mortgage after an IVA, even with a damaged credit file, if you know what lenders are looking for and where to turn for the right help.

Getting a mortgage with an IVA isn’t always easy, but it’s far from impossible. With guidance from specialist lenders, a clean track record since your IVA ended and a decent mortgage deposit, you may have more options than you think.

How an IVA Affects Your Credit and Mortgage Eligibility

An IVA is a legally binding agreement between you and your creditors to repay part of what you owe over time. It’s one of the most common forms of debt relief in the UK and usually runs for five to six years. While it can provide an affordable payment plan, it also leaves a clear mark on your credit file, affecting your ability to secure future credit including a mortgage loan.

When you apply to get a mortgage, lenders will review your credit report, your full credit history and often your credit rating. If they see an active or recent IVA, many will either reject the application outright or offer less favourable interest rates.

That said, some specialist mortgage lenders are more open-minded. They consider the full context and not just your past, but your income, current commitments and how well you’ve managed money since your IVA.

Can You Get a Mortgage During an IVA?

Applying for a mortgage with an IVA still in place is extremely difficult. You’d need written approval from your insolvency practitioner, even then most high street mortgage lenders would still decline you.

A few specialist lenders may consider niche cases, but it’s rare. Most people choose to wait until their IVA has been fully completed before making a mortgage application, which opens up more affordable and realistic options.

Getting a Mortgage After an IVA Ends

Once your IVA is marked as complete, you can technically start applying for a mortgage right away, however your success will depend on how you’ve managed your finances since.

Lenders will still see your IVA on your credit record for up to six years from the start date. If you’ve kept on top of bills, rebuilt your credit rating and avoided further debt, you’ll stand a much better chance of being approved.

To get a mortgage in this situation, most brokers recommend having a larger mortgage deposit and working with lenders who regularly deal with people who’ve had IVAs or bad credit mortgages in the past.

Can You Get a Joint Mortgage with an IVA on Your Record?

Joint applications are common, especially for first-time buyers. If one applicant has an IVA on their credit file, it will influence how a lender views the overall risk, even if the second applicant has perfect credit.

While some mortgage lenders may hesitate, others are open to it if your financial picture is otherwise strong. A larger deposit, consistent income and no recent defaults help improve the chances of approval. It also helps if you work with a mortgage broker who understands how to position a joint mortgage with adverse credit.

What Happens at Mortgage Renewal if You’ve Had an IVA?

If you already own a home, you might be concerned about how an IVA could affect your mortgage renewal. Whether or not your IVA causes a problem depends on the lender’s criteria and whether they run a full credit check.

Some lenders allow renewals without checking your credit history again, particularly if you’re staying on the same deal. If you’re remortgaging with a new provider, the IVA may limit your options or affect the interest rates offered.

Why Specialist Lenders Are Key After an IVA

Not all mortgage lenders assess applications the same way. While the big banks often reject applicants with any adverse credit, specialist lenders focus more on your financial situation now. They take a broader view of your affordability and consider factors beyond your credit score alone.

These lenders don’t always advertise to the public and are usually accessed through a mortgage broker or IVA mortgage advisor. They understand the nuances of IVAs and offer tailored products that suit buyers coming out of financial recovery.

How a Mortgage with IVA Calculator Can Help You Plan

Using a mortgage with IVA calculator gives you a ballpark idea of what borrowing might look like, including potential loan size and monthly repayments. While it won’t replace formal advice, it helps set expectations around affordability and what a lender may offer.

Just be careful with generic calculators, they often assume clean credit and don’t reflect the specific conditions that apply when you’ve had an IVA or other poor credit issues.

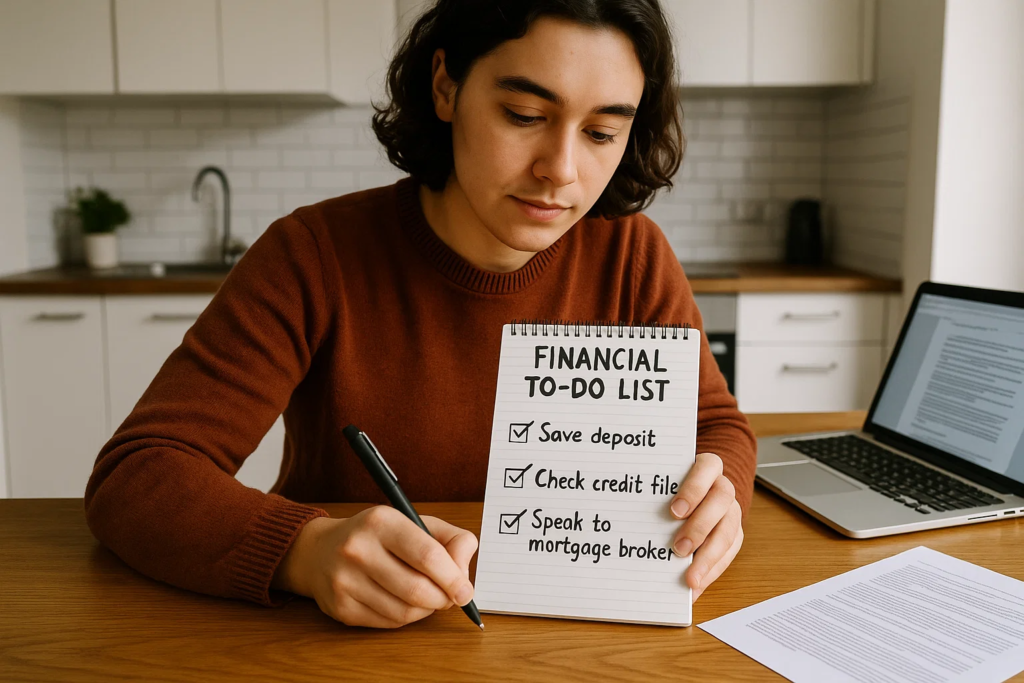

What Makes a Successful Mortgage Application After an IVA?

Success often comes down to preparation. If you’ve rebuilt your credit, kept up with all your monthly payments and shown financial discipline, you’re already ahead.

Lenders want to see a track record of stability. That means consistent employment, responsible use of credit and no missed bills. Saving a larger deposit also makes a difference, not just because it lowers the risk for the lender, but because it shows you’ve made progress since your IVA.

Why a Broker Is Often Essential for IVA Mortgages

If you’re dealing with past debt problems, you’ll benefit from working with a mortgage broker who understands IVA mortgage cases. These brokers know which IVA mortgage lenders are open to your situation and how to structure an application for the best chance of approval.

They’ll also help you avoid applying to lenders who will almost certainly decline, preventing further damage to your credit file from unnecessary hard searches.

Will You Pay Higher Interest Rates After an IVA?

In most cases, yes. Lenders offering mortgages with an IVA generally charge higher interest rates than those available to borrowers with clean credit.

However, those rates aren’t permanent. Once you’ve made timely repayments for a couple of years, you may be able to remortgage to a more competitive deal, especially if your credit record has improved and the IVA has dropped off your report.

While you may have to pay fees up front or accept less flexible terms in the beginning, these are stepping stones to better options down the line.

Does an IVA Affect Your Mortgage Forever?

An IVA stays on your credit report for six years, but its impact lessens with time, especially if you’ve been proactive in rebuilding your credit. If you’re beyond that six-year window and have kept your finances in check, many lenders won’t see it as a major issue.

It also depends on how long ago the IVA was completed. A fresh IVA will still affect most mortgage applications, but one that ended years ago is less likely to be a barrier, particularly with the help of a specialist mortgage lender.

Can You Really Get a Mortgage with an IVA?

The simple answer is yes, you can get a mortgage after an IVA. It may take more effort, involve higher costs early on and require help from an experienced mortgage broker, but it’s not out of reach. With the right support, a clear plan and time on your side, homeownership is still possible even after financial difficulties.

What matters most is how you’ve handled your money since the IVA ended. Lenders know that people face challenges, what they want to see is that those challenges are behind you and that you’re now in control.