May not be suitable in all circumstances. Fees apply read more. Your credit rating may be affected, read more.

For free, independent advice, you should visit to Money Helper via their website.

For free, independent advice, you should visit to Money Helper via their website.

How much does an IVA cost?

There is no application fee when you apply for help with My Debt Plan

No upfront fees are required, and in the event your IVA application is rejected there will be no charge

All information we provide during the initial IVA process to get it set up is free of charge

If you are eligible and you decide an IVA is the best option for you, we will put together a proposal to your creditors and will share full details of all the costs that will be included in your IVA agreement.

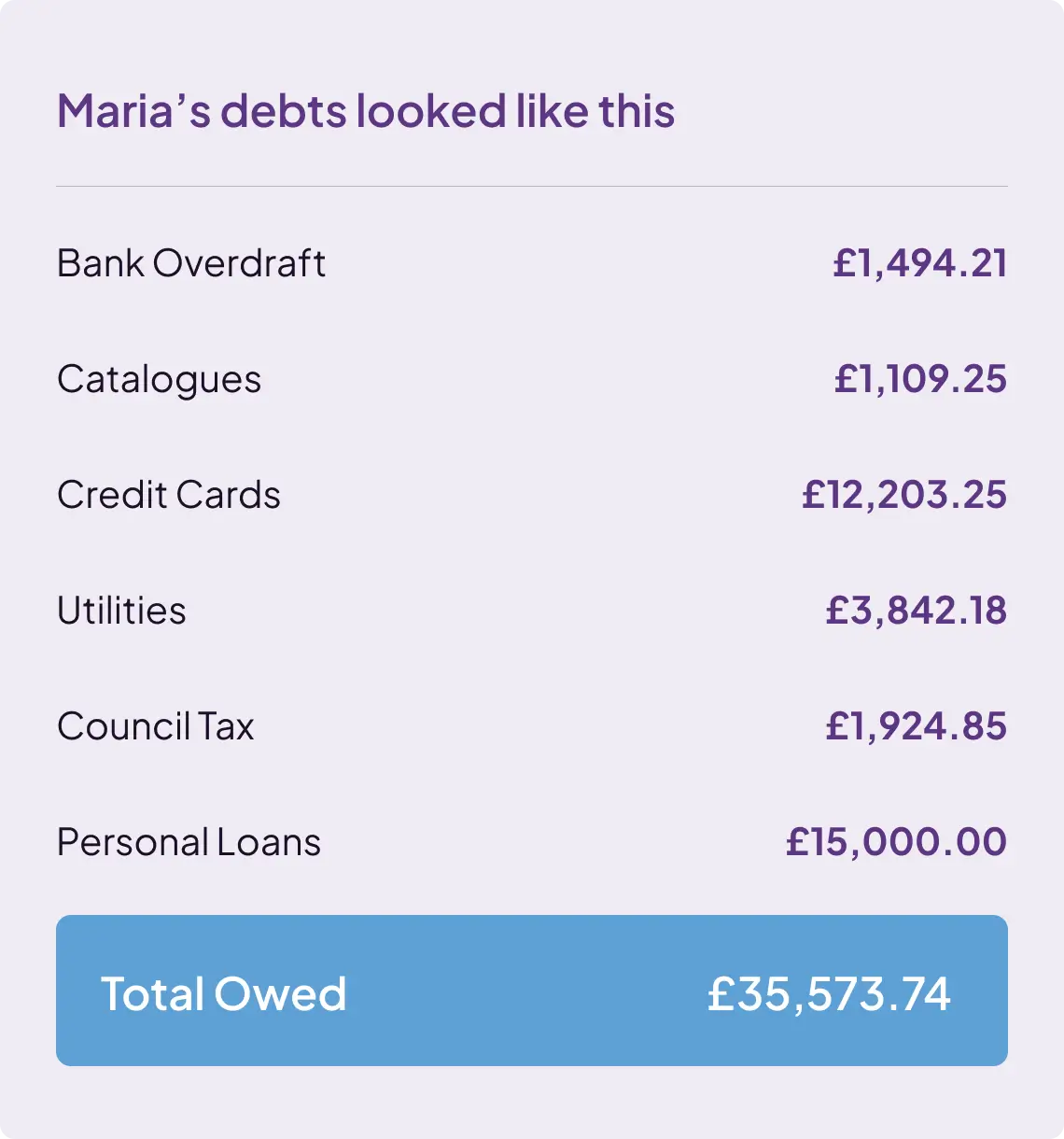

Here's how we helped Maria write-off 70% of her total debt of £35,573.74

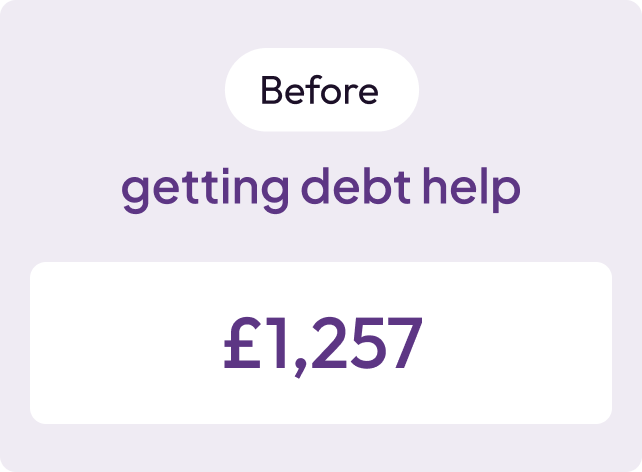

How her monthly repayments looked like after our help

*Monthly payment based on individual financial circumstances *Example is based on period of 60 months. *Credit rating may be affected, and fee may apply. *Subject to creditor acceptance

What fees are involved in an IVA?

All fees paid are charged from the monthly contributions you make into the IVA and are not in addition.Costs will only be recovered on approval of your arrangement and once you commence making payments to it. The fees involved are:

Nominee’s fees:

This fee covers the preparation of the proposal to the creditors and calling the meeting for creditors to vote the approval of an IVA case.

At My Debt Plan we charge a fixed Nominee’s fee of £1750.

Supervisor’s fees:

These are the fees that cover the administration work involved to keep the arrangement running once the IVA is approved. It will cover things such as the registration fee, statutory insurance, disbursements and annual reviews of your IVA.

At My Debt Plan we charge a fixed Supervisor’s fee of £1,900 regardless of the amount of your monthly contribution.

We will charge an additional 15% on any other asset realisations that may come into your arrangement, for example, windfalls or compensation for miss-selling claims.

For an IVA arrangement with My Debt Plan, the total of all of these fees is £3,650 although this may be adjusted by creditors when they vote on whether to accept. No matter what the end total of costs come to, you can be rest assured that these will be taken from the monthly payment we agree with you, and you won’t notice these fees being taken at all.

IVA Fees explained

If your IVA is terminated because e.g. you have failed to pay all the agreed IVA payments, it is likely that the majority of the contributions you have paid will have been used to pay the costs and expenses of your IVA. This will mean that the amounts you owe to your creditors will have reduced by very little. Your creditors will again be able to claim the amounts you owe to them together with interest and charges

Debt Solutions

What is an IVA and how does it work?

An IVA (Individual Voluntary Arrangement) is a formal debt solution that allows you to make reduced payments towards your debts over a fixed period, usually five to six years. It’s a legally binding agreement between you and your creditors.

What Happens If I Can't Afford The IVA Fees?

If you’re struggling to afford the IVA fees, it’s important to discuss your concerns with your insolvency practitioner as soon as possible. They might be able to make adjustments or provide guidance on alternative solutions.

Are There Any Hidden Charges I Should Be Aware Of?

No, reputable insolvency practitioners My Debt Plan are transparent about their fees. All charges associated with the IVA will be clearly outlined in the agreement, and you should have a clear understanding of what you’re paying for.

Can I Get A Breakdown Of The IVA Fees?

Absolutely. Reputable insolvency practitioners will provide you with a detailed breakdown of all fees associated with the IVA. This breakdown should be clear and easy to understand.

An Individual Voluntary Arrangement (IVA) is a formal agreement with creditors to repay a portion of your debts over time, but it does have an impact on your credit score and it will be difficult to obtain further credit whilst on an IVA. Once an IVA is approved, it is recorded on your credit report and will typically remain there for six years from the date it starts. However, it’s important to note this is the case for most debt solutions and your credit score will likely already have been affected by being in debt in the first place. Once your IVA is complete you will get a fresh start to begin rebuilding your credit rating.

Fees

IVA costs are charged for the preparation of your proposal and the administration of the arrangement for the full term (usually 5 years) these costs are charged from the monthly contributions you make into the IVA and are not in addition. Costs will only be recovered on approval of your arrangement and once you commence making payments to it. The fees for preparation of the proposal to creditors and calling the meeting for creditors to vote on its approval are called nominees fees, the fees for running the arrangement once approved are called supervisors fees. There are also some expenses incurred in the running of the arrangement such as the registration fee and the statutory insurance that needs to be taken by law, these are called disbursements. For our arrangements, the total of all of these is £3,650 although this may be adjusted by creditors when they vote on whether to accept. No matter what the end total of costs come to, you can be rest assured that these will be taken from the monthly payment we agree with you.

For free, independent advice, you should visit to Money Helper via their

For free, independent advice, you should visit to Money Helper via their